All Categories

Featured

Table of Contents

The are entire life insurance policy and universal life insurance policy. The cash value is not added to the fatality benefit.

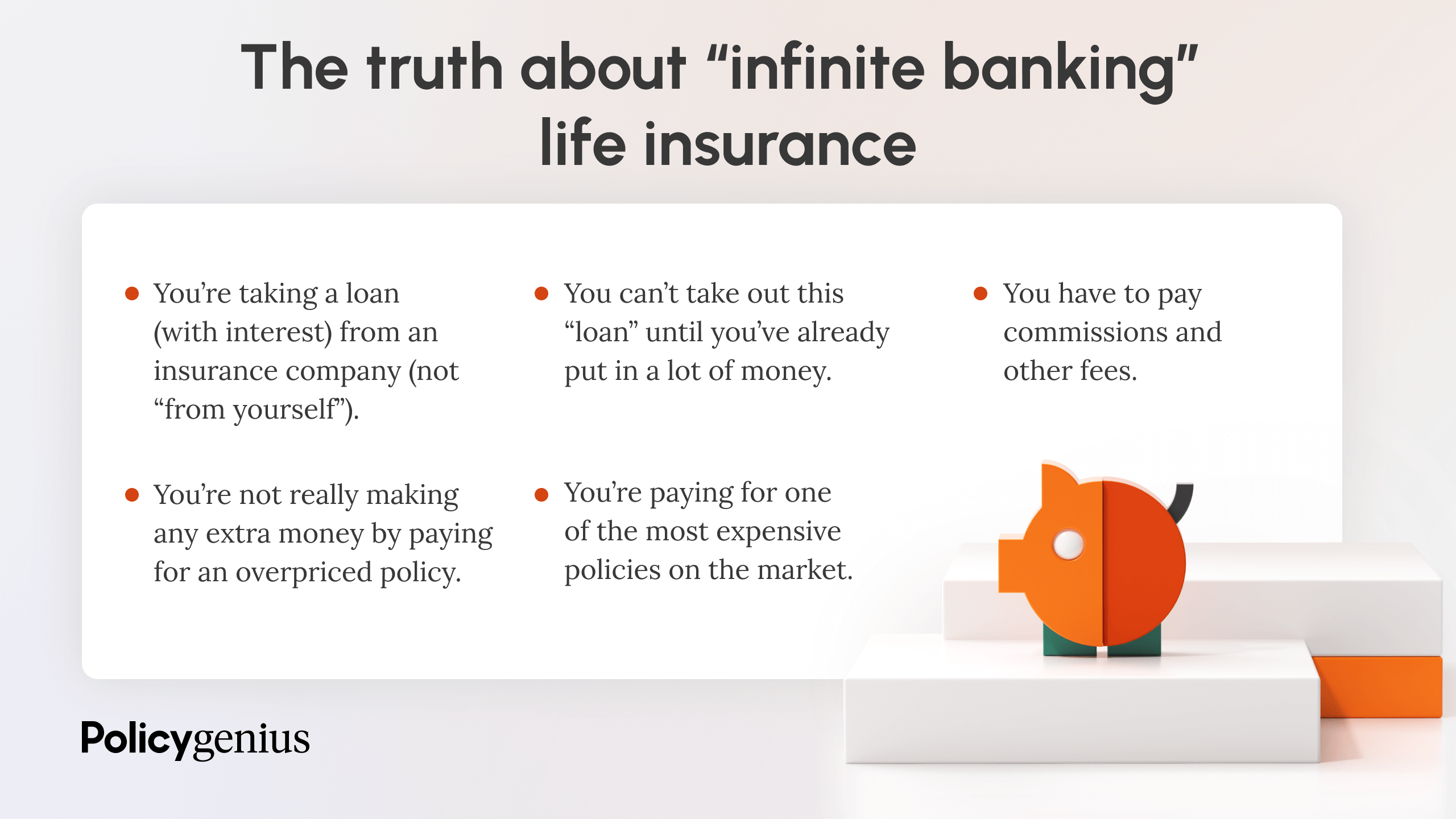

After ten years, the money worth has grown to roughly $150,000. He gets a tax-free car loan of $50,000 to start a service with his sibling. The policy finance rate of interest is 6%. He pays off the lending over the following 5 years. Going this course, the rate of interest he pays returns into his plan's money value instead of a monetary institution.

Ibc Finance

Nash was a financing expert and fan of the Austrian school of business economics, which supports that the value of items aren't explicitly the result of traditional financial frameworks like supply and demand. Instead, people value cash and items in different ways based on their financial condition and needs.

One of the risks of typical financial, according to Nash, was high-interest prices on fundings. Too numerous people, himself consisted of, entered into monetary problem because of dependence on financial institutions. Long as banks set the passion rates and financing terms, individuals didn't have control over their very own riches. Becoming your own lender, Nash figured out, would certainly place you in control over your economic future.

Infinite Banking requires you to possess your monetary future. For goal-oriented people, it can be the most effective economic tool ever before. Here are the benefits of Infinite Financial: Arguably the solitary most helpful aspect of Infinite Financial is that it enhances your cash circulation. You don't need to experience the hoops of a conventional bank to get a funding; simply demand a policy loan from your life insurance policy business and funds will certainly be provided to you.

Dividend-paying whole life insurance is very reduced danger and provides you, the policyholder, a lot of control. The control that Infinite Financial supplies can best be organized right into 2 categories: tax obligation benefits and property defenses - rbc infinite visa private banking. One of the reasons entire life insurance policy is suitable for Infinite Banking is exactly how it's tired.

Infinite Banking Uk

When you use whole life insurance coverage for Infinite Banking, you enter into an exclusive agreement between you and your insurance coverage business. These protections may differ from state to state, they can consist of defense from property searches and seizures, defense from reasonings and security from creditors.

Entire life insurance policy plans are non-correlated properties. This is why they work so well as the monetary structure of Infinite Banking. No matter of what takes place in the market (supply, actual estate, or otherwise), your insurance policy preserves its well worth.

Market-based financial investments expand wide range much faster yet are exposed to market fluctuations, making them naturally high-risk. What happens if there were a third bucket that offered safety yet additionally modest, guaranteed returns? Entire life insurance policy is that third container. Not only is the price of return on your whole life insurance policy plan guaranteed, your survivor benefit and costs are also assured.

This structure aligns completely with the principles of the Continuous Wealth Approach. Infinite Banking charms to those seeking higher monetary control. Right here are its main advantages: Liquidity and accessibility: Plan car loans supply instant access to funds without the constraints of standard small business loan. Tax effectiveness: The cash value grows tax-deferred, and plan lendings are tax-free, making it a tax-efficient tool for developing riches.

Bank On Yourself Program

Property security: In several states, the cash value of life insurance is shielded from financial institutions, adding an added layer of financial safety and security. While Infinite Banking has its values, it isn't a one-size-fits-all option, and it includes significant downsides. Right here's why it may not be the finest approach: Infinite Financial commonly needs elaborate plan structuring, which can puzzle insurance policy holders.

Visualize never ever having to worry regarding bank financings or high passion rates once more. That's the power of limitless banking life insurance coverage.

There's no set car loan term, and you have the flexibility to choose the payment routine, which can be as leisurely as paying off the financing at the time of fatality. This adaptability encompasses the servicing of the lendings, where you can choose interest-only repayments, maintaining the lending balance level and convenient.

Holding cash in an IUL repaired account being attributed passion can often be better than holding the money on down payment at a bank.: You've constantly desired for opening your own bakeshop. You can obtain from your IUL plan to cover the initial expenses of leasing an area, buying equipment, and employing staff.

Life Insurance Concept

Personal lendings can be gotten from standard financial institutions and credit unions. Below are some vital factors to take into consideration. Bank card can provide a versatile method to obtain money for really temporary periods. Borrowing money on a credit card is generally very expensive with annual percent prices of passion (APR) usually getting to 20% to 30% or even more a year.

The tax obligation therapy of policy loans can vary dramatically relying on your country of house and the details terms of your IUL policy. In some areas, such as North America, the United Arab Emirates, and Saudi Arabia, policy lendings are generally tax-free, supplying a significant benefit. Nonetheless, in other territories, there may be tax ramifications to take into consideration, such as possible tax obligations on the funding.

Term life insurance coverage just provides a death benefit, without any kind of money worth build-up. This suggests there's no cash money value to borrow against.

However, for funding officers, the considerable regulations enforced by the CFPB can be viewed as cumbersome and limiting. Initially, funding policemans typically argue that the CFPB's guidelines create unnecessary bureaucracy, resulting in even more documentation and slower loan processing. Guidelines like the TILA-RESPA Integrated Disclosure (TRID) guideline and the Ability-to-Repay (ATR) demands, while aimed at securing consumers, can result in hold-ups in shutting deals and boosted operational costs.

{kind=link}

Latest Posts

'Be Your Own Bank' Mantra More Relevant Than Ever

Whole Life Insurance-be Your Own Bank : R/personalfinance

Private Family Banking Life Insurance